The United States just marked its 250th anniversary, so it’s a natural time to revisit one of the country’s most enduring ideas: the American Dream of homeownership.

Today, 81% of U.S. adults still say owning a home is part of that dream, according to a June 2026 survey commissioned by Newrez.

For generations, homeownership has been tied to independence, stability and long-term financial growth. But in today’s market, with home prices increasing over the last few years, that may look different than it did for previous generations.

If you’re interested in learning what home loans might be available for you, a Newrez mortgage expert can help walk you through your options.

Click to navigate:

- First-Time Homebuyers Continue To Be a Major Driver of the Purchase Market

- Repeat Buyers

- Inflation from 2022 to 2025

- Practical Takeaways for 2026 Buyers

- The Bottom Line

- FAQs

First-Time Homebuyers Continue To Be a Major Driver of the Purchase Market

First-time buyers often face some of the steepest barriers to purchasing a home. Unlike repeat buyers, they typically are not bringing equity from a previous home into the transaction. That means relying more heavily on savings, family support or homebuyer assistance programs to cover upfront costs like the down payment.

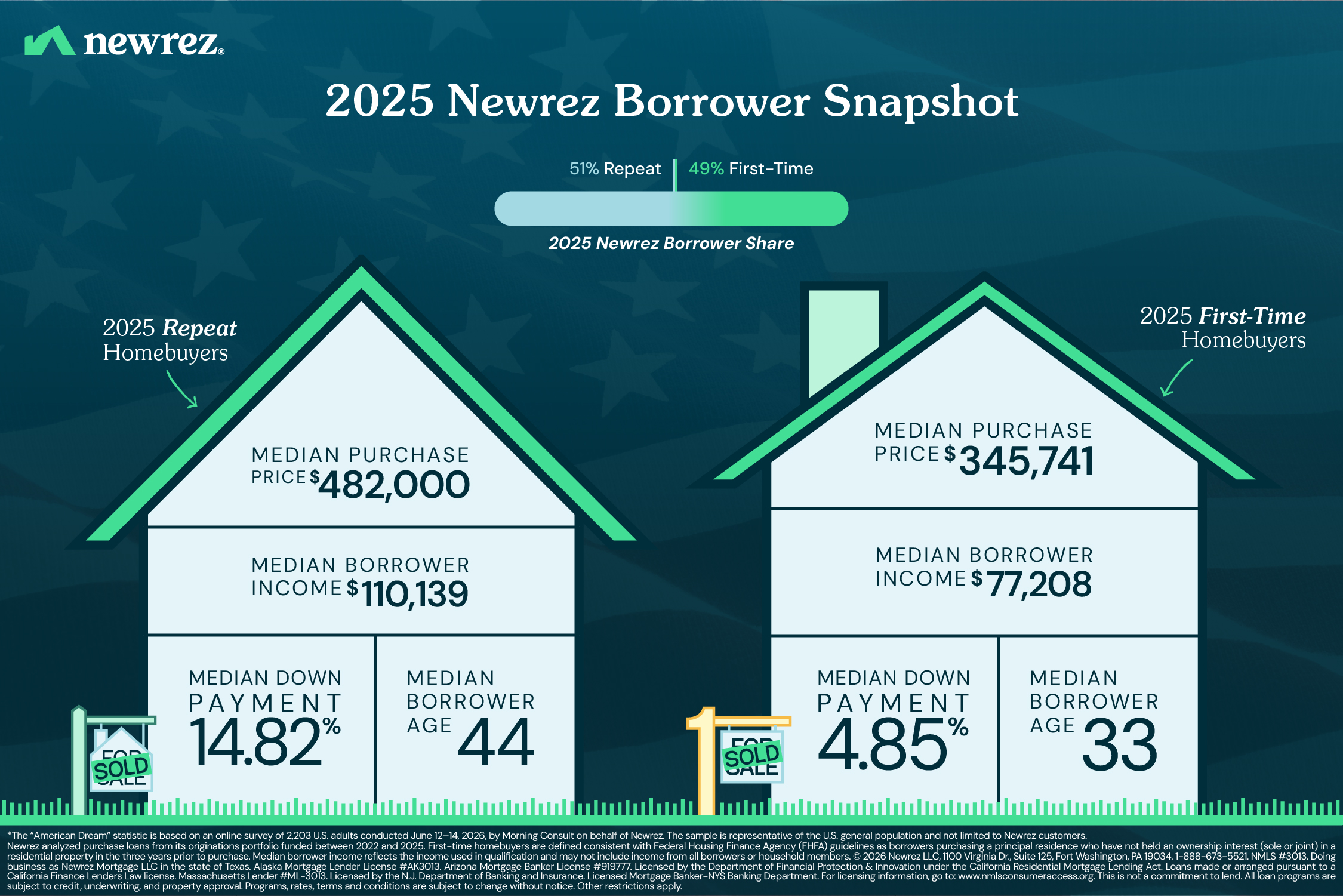

Even with these challenges, first-time homebuyers remain a major part of the market. Newrez originations data from 2022 through 2025 shows that first-time homebuyers represented 56% of borrowers in 2022 and had declined to 49% by 2025. Although the share of first-time homebuyers declined, they still made up nearly half of all purchase loan activity in 2025. The median age for first-time buyers remained steady at 33.

Newrez First-Time Buyer Data

| Metric | 2022 | 2023 | 2024 | 2025 | Change |

| First-Time Buyer (FTB) Share | 56% | 53% | 49% | 49% | -7 points |

| FTB Median Age | 33 |

33 |

33 |

33 |

0 |

| FTB Median Down Payment | 5.00% |

5.00% |

5.00% |

4.85% |

-0.15 points |

| FTB Median Purchase Price | $314,000 | $293,921 | $326,000 | $345,741 | +10% |

| FTB Median Borrower Income | $61,728 | $65,000 | $71,158 | $77,208 | +25% |

Purchase prices for first-time buyers increased 10% over the period, which may reflect a rising cost environment that first-time buyers must navigate.

Because they typically have lower incomes and fewer financial reserves than repeat buyers, first-time buyers may be more sensitive to changes in pricing, rates and monthly costs.

First-time buyer down payments remained near 5%, less than what repeat buyers typically put down. Even though costs are increasing, first-time buyers are still taking advantage of low down payment options to enter the market.

Repeat Buyers

Repeat buyers make up a growing share of Newrez borrowers and often enter the purchase process with more resources than first-time buyers. A narrow majority of purchase loans are now taken out by repeat buyers.

Newrez Repeat Buyer Data

| Metric | 2022 | 2023 | 2024 | 2025 | Change |

| Repeat Buyer Share | 44% | 47% | 51% | 51% | +7 points |

| Repeat Buyer Median Age | 42 |

43 |

43 |

44 |

+2 years |

| Repeat Buyer Median Down Payment | 15.00% |

15.00% |

15.00% |

14.82% |

-0.18 points |

| Repeat Buyer Median Purchase Price | $432,620 | $417,245 | $460,000 | $482,000 | +11% |

| Repeat Buyer Median Borrower Income | $87,526 | $92,628 | $103,992 | $110,139 | +26% |

Even though costs are increasing, repeat buyers are still putting down around 15% of the purchase price.

The age of repeat buyers has increased slightly while the age of first-time homebuyers has stayed stable.

Inflation from 2022 to 2025

When comparing borrower characteristics from 2022 to 2025, it's important to recognize that the broader economy changed during that period as well. The Newrez originations data in this report has not been adjusted for inflation, and the table below provides additional context on inflation trends in the U.S. over the same timeframe.

| Year | Inflation increase from the previous year |

| 2022 | +8% |

| 2023 |

+4.1% |

| 2024 |

+2.9% |

| 2025 | +2.6% |

*Table data sourced from the Federal Reserve Bank of Minneapolis1.

Practical Takeaways for 2026 Buyers

Here are a few tips for buyers thinking about purchasing a home in 2026:

- Focus on the full monthly payment, not just the purchase price: Rising home prices are only one part of affordability. Taxes, insurance, interest rates and ongoing homeownership costs all play a role in your monthly expenses.

- Be intentional about your down payment strategy: A higher down payment can reduce your loan balance and monthly payment, but it’s equally important to maintain cash reserves for unexpected expenses after closing.

- Understand that while market conditions may be stabilizing, costs remain elevated: While some income and pricing trends have leveled off recently, overall affordability challenges are still present. Buyers should plan for a market that is steadier than it used to be, not necessarily inexpensive.

- Get preapproved* before you start shopping: A mortgage preapproval can give you a clearer picture of what you can realistically afford. It can also make your offer more competitive once you find a home, since sellers often view preapproved buyers as more prepared and reliable.

- Look into assistance programs: Check out down payment assistance, grants and first-time buyer programs to see if they can reduce upfront costs.

The Bottom Line

Homeownership is still within reach, but it may require more planning than it did in the past. Explore assistance programs, see what monthly mortgage payment you can afford and what loan amount you can qualify for before you begin to shop.

If you’re thinking about buying a home, Newrez can help you navigate your options every step of the way. Reach out to one of our loan experts today to get started—our mission is to do everything possible to make home happen.

FAQs

Yes. Newrez data shows first-time buyers remained a significant share of funded purchase borrowers in 2025, even though their share declined from 2022 levels.

No. In 2025, Newrez borrowers who were first-time buyers had a median down payment of 4.85%, and repeat buyers had a median down payment of 14.82%. A 20% down payment can help reduce the loan amount, but it is not required. If you have a down payment of less than 20% on a conventional loan, you’ll need to pay for private mortgage insurance (PMI). Before deciding on the size of your down payment, consider how it will impact your future monthly payments (including the added cost of PMI) and your cash reserves.

The best first step is to get preapproved before shopping. That way, homebuyers will have a better understanding of what they can afford, and what their monthly payment might look like before they start shopping.