Homeowners are facing a steep rise in the cost of homeowners insurance—and the impact is being felt in nearly every region of the U.S.

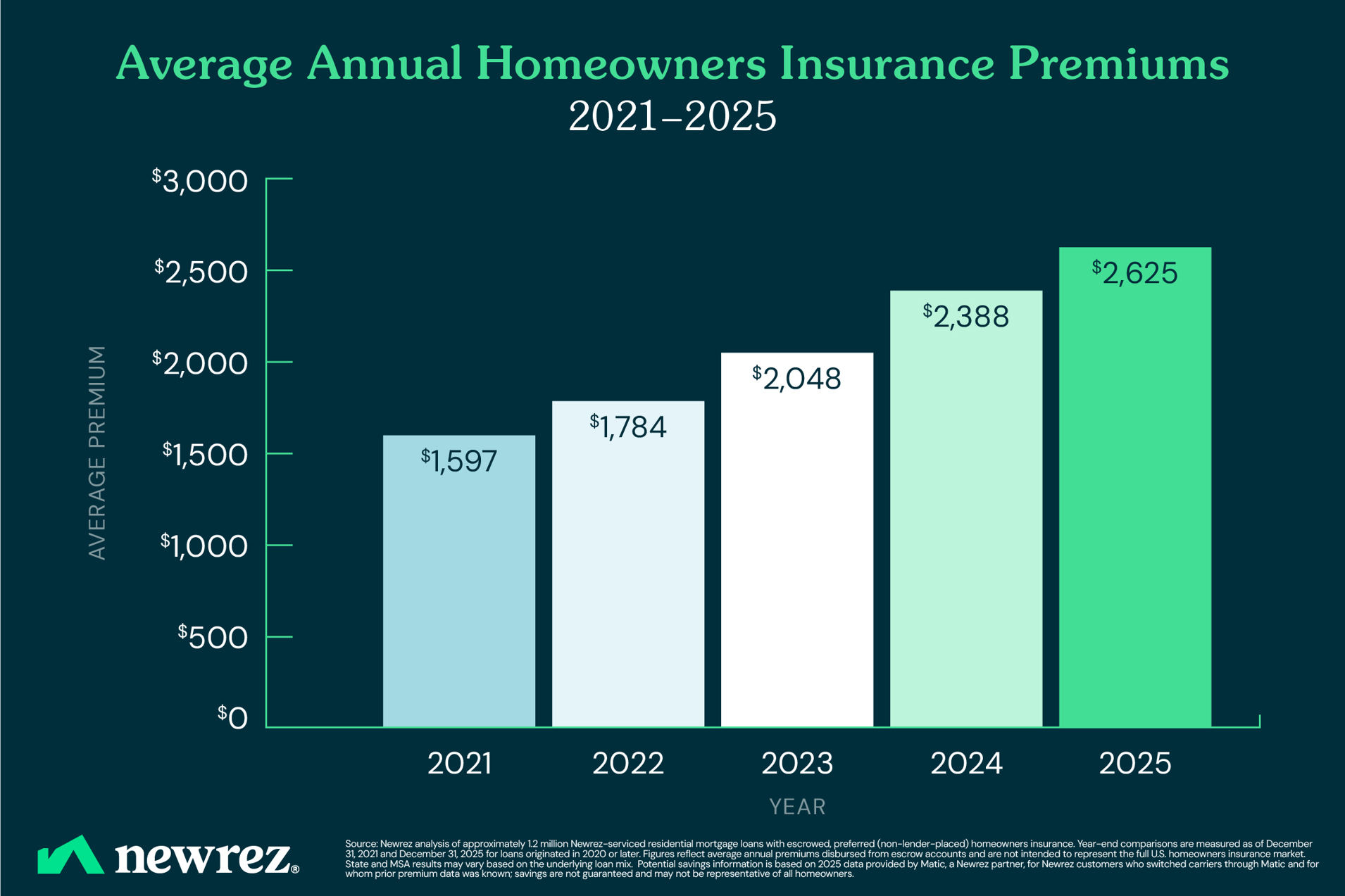

Newrez mortgage servicing data shows that insurance premiums tied to borrower escrow accounts rose 64% on average between year‑end 2021 and year‑end 2025. In contrast, premiums increased a more modest 17% between 2016 and 2020.

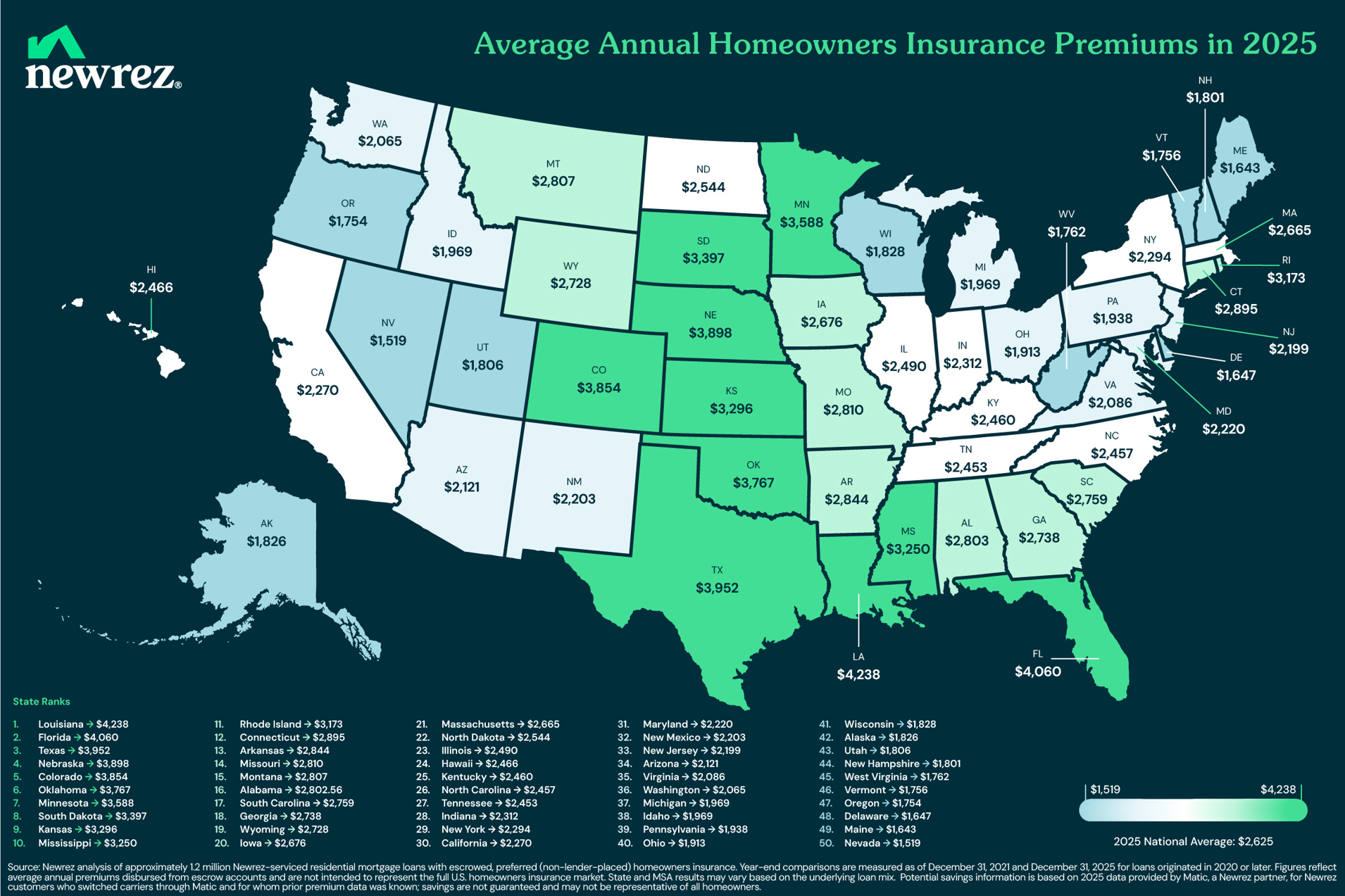

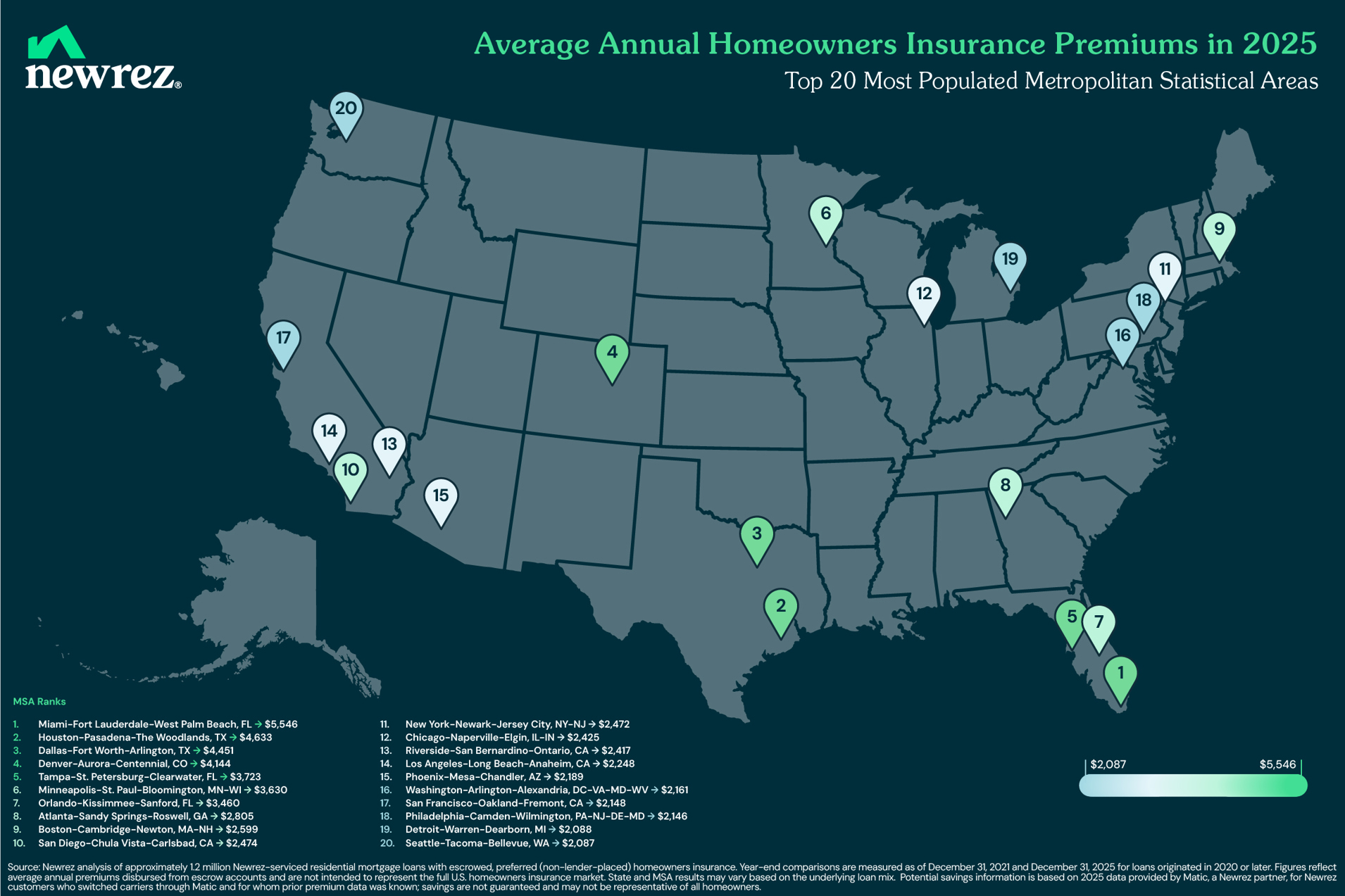

According to the analysis of roughly 1.2 million Newrez‑serviced loans originated in 2020 or later, the average national annual homeowners insurance premium reached $2,625 at the end of 2025, up from $1,597 in 2021.

This creates challenges not only for homeowners, but for people considering making a purchase, since insurance is typically required to close a mortgage.

Shopping around for a great deal on homeowners insurance has never been more important. With Newrez’s insurance partner Matic, borrowers can review multiple quotes in minutes and potentially save hundreds. According to 2025 data from Matic, Newrez customers who switched insurance carriers through Matic and for whom prior premium data was known saved an average of $928.*

This article brings together Newrez’s latest data with some basic homeowners insurance knowledge so homeowners and homebuyers can better navigate shifting insurance costs and make smart choices for their homes, their families and their finances.

If you’re looking for a mortgage lender with the know-how to help you select a great loan, give our mortgage experts a call so we can make home happen for you.

Table of Contents

- What Is Homeowners Insurance?

- What Could Be Causing This Trend?

- A Breakdown of Homeowners Insurance Coverage

- What Is Not Covered by Homeowners Insurance?

- Factors That May Influence State-Level Insurance Costs

- Disaster and Climate Risk Coverage

- How Homeowners Insurance Works With Your Mortgage

- FAQs About Homeowners Insurance

- Methodology

What Is Homeowners Insurance?

Homeowners insurance typically protects the structure of the home, personal belongings, and liability, and it’s typically required by mortgage lenders. Because premiums are often paid through escrow, changes in insurance costs flow directly into a homeowner’s monthly mortgage payment.

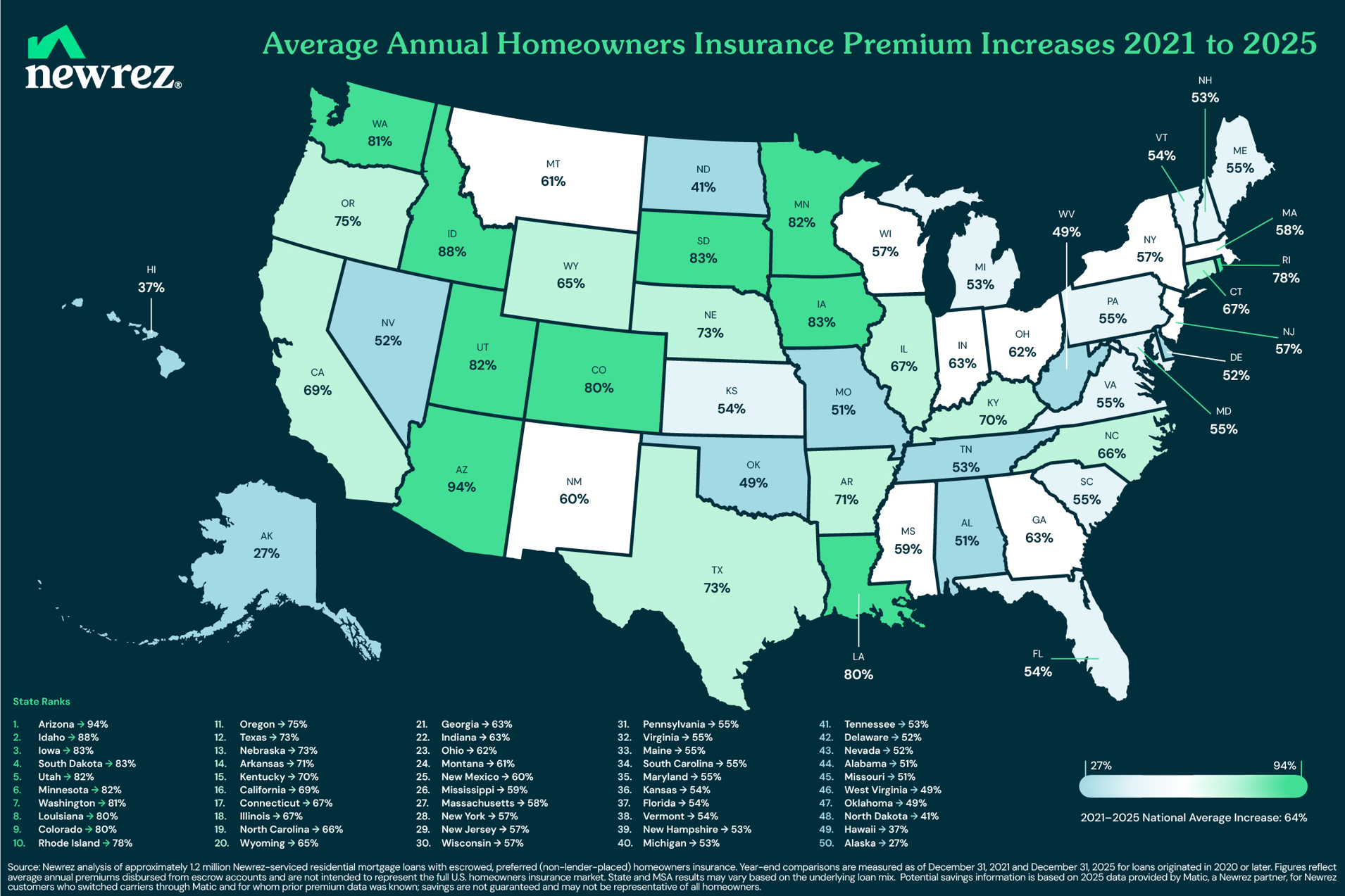

The Data: Growth Patterns Over 5 Years Vary Widely by State

While rising insurance costs have become a national trend, the degree of increase differs dramatically by state. Several of the largest increases occurred in western and central states, including:

- Arizona: +94%

- Idaho: +88%

- Iowa: +83%

- South Dakota: +83%

- Utah: +82%

- Minnesota: +82%

- Washington: +81%

- Louisiana: +80%

- Colorado: +80%

States with large populations also experienced drastic increases. For example:

(In order of largest population)

- California: +69%

- Texas: +73%

- Florida: +54%

- New York: +57%

- Pennsylvania: +55%

- Georgia: +63%

Even states that saw comparatively smaller increases in insurance costs still experienced meaningful growth. For example, Alaska saw the lowest increase at 27%, while many Midwestern and Southern states still experienced increases between 50% and 70%.

What Could Be Causing This Trend?

It’s likely not just one factor that’s causing insurance costs to climb, as prices are impacted by various economic, housing and climate circumstances. But here are a few elements that could be putting particular pressure on insurance prices:

- Increased Frequency and Severity of Natural Disasters: The U.S. Department of Treasury reports that climate-related events are increasing the cost of homeowners insurance across the country, as insurers have faced higher losses and greater exposure to catastrophic events.1 Areas prone to disaster risk could see heftier increases.

- Higher Rebuilding and Construction Costs: Elevated construction costs and supply chain challenges have likely affected premiums, as insurers usually have to price policies to reflect the increased cost of repairing or replacing homes after a covered loss.2

- Inflation in Labor and Materials: Persistent inflation in building materials and labor has raised the cost of claims, pushing up premiums. In particular, the staggering inflation seen post-COVID had an outsized impact.2

- Regional Insurance Market Risks and Underwriting Changes: If the number of claims filed in your area has increased, this may be caused by location-specific risks, which insurers often take into account when they price policies. And if some insurers have pulled away from your area, then the remaining insurers might make their underwriting guidelines stricter to protect themselves from risk—and may up their prices.

Matic Co-Founder and CEO Ben Madick acknowledged the influence of weather-related catastrophes, increasing rebuilding costs and regulatory constraints on steep cost increases.

“Most policies are ‘replacement cost’ policies, meaning the insurer must pay what it costs to rebuild your home for today, not what you paid for it years ago,” he explained, adding that both inflation and tariffs have played a role.

Coastal states like Louisiana, Florida and Texas regularly rank among the most expensive states because they face elevated hurricane and coastal storm risk, Madick said, but he’s also not surprised to see sharp price increases in some landlocked states.

“Some of the most costly insurance losses actually come from severe convective storms, which produce hail, wind and tornadoes, and are very common across the Plains and Mountain West,” Madick said. “States like Nebraska and Colorado experience frequent hail events that can cause widespread roof and property damage, and those losses have pushed premiums higher in recent years. In Colorado, additional risk factors such as wildfires and population growth have also contributed to rising premiums.”

Some Midwest states have seen significant price growth simply because they’ve historically had relatively low premiums, Madick said, and insurers are now reacting to rising risk and rebuilding costs.

A Breakdown of Homeowners Insurance Coverage

While every policy is a little different, most standard plans include a few core types of coverage that work together to safeguard you and your property. Most insurance plans provide:

- Dwelling Coverage: Helps pay for repair or rebuild of the physical structure of your home in the event of storms, a fire, vandalism or falling branches.

- Protection for Your Personal Belongings in the Home: Helps if your things suffer smoke or fire damage, water damage, or even if they’re stolen.

- Personal Liability Coverage: Important if someone suffers an injury on your property, or if you damage someone else’s property. Usually covers legal expenses, medical expenses and settlement payments.

- Loss of Use Coverage: Covers the cost of living elsewhere if your home becomes uninhabitable after a covered event. Typically covers the cost of a hotel stay and related expenses.

Coverage limits deductibles vary depending on the insurance policy and provider.

Has your property been damaged or lost in a disaster? Learn more about how to file an insurance claim.

What Is Not Covered by Homeowners Insurance?

Although homeowners insurance covers many common risks, some events and situations are usually not included in standard policies.

Common exclusions may include:

- Flood Damage: Separate flood insurance may be required for certain natural disasters, covered in our ‘Disaster and Climate Risk Coverage’ section below.

- Normal Wear and Tear: Insurance doesn’t generally cover the typical damage that occurs to a property as it ages.

- Pest Infestations: Damage from termites or rodents is considered a maintenance issue, not a matter for insurance.

- Maintenance-Related Issues: Problems caused by neglect such as mold, a slow leak or failing to make repairs are usually not covered.

Average Homeowners Insurance Costs by State

Homeowners insurance costs vary widely from one location to another, largely because insurers price policies based on the level of risk in a given area.

Factors that may influence state-level insurance costs include:

- Exposure to natural hazards such as hurricanes, wildfires, tornadoes or severe storms

- Flood risk, especially in coastal or low-lying areas

- Local rebuilding costs, which can be influenced by labor shortages or material prices

- Local claim frequency, which can be pushed up by area crime and other factors

Disaster and Climate Risk Coverage

Homeowners in some areas may need extra protection beyond what a standard policy provides. In higher-risk regions, lenders may require additional coverage to ensure the property is adequately protected.

- Flood damage is usually covered through a separate flood insurance policy

- Earthquake coverage may be offered as an add-on by your insurance

- Hurricane or windstorm coverage may require additional riders in certain coastal areas

- Wildfire coverage may depend on location and policy structure

Homeowners living in higher-risk regions should review their coverage carefully and consult their insurance provider about available options.

How Homeowners Insurance Works with Your Mortgage

Homeowners insurance and your mortgage go hand in hand. Because your home serves as collateral for your loan, lenders want to be sure your home is protected from the moment you take ownership.

Why Do Mortgage Lenders Require Homeowners Insurance?

Lenders require insurance so that in the event the home is damaged, there are funds to repair or rebuild it. This protects both you and your lender’s investment.

Can You Close on a House Without Insurance?

In most cases, no. Most lenders require proof of an active homeowners insurance policy before you can close.

When Does Homeowners Insurance Kick In?

After securing insurance, coverage usually begins on the closing date of the home purchase, so the property is protected from the moment ownership transfers to you.

Do You Need Insurance Before Underwriting Approval?

Insurance is typically finalized before closing rather than during the initial underwriting review. However, lenders may ask for confirmation that coverage will be in place before the loan is funded.

How Does Homeowners Insurance Affect Closing Costs?

Homebuyers often pay the first year’s premium upfront at closing. In many cases, additional funds may also be collected to establish an escrow account for future insurance payments.

Wondering what monthly costs will come to for your dream home? Use our mortgage payment calculator.

Escrow and Homeowners Insurance

Like many homeowners, you may pay homeowners insurance from an escrow account kept by your lender.

What Is an Escrow Account?

A loan servicing escrow account is an account provided by your lender that you pay into regularly as a part of your mortgage payment. When your homeowners insurance and property tax bills come due, your lender pays them on your behalf from the money held in this account. Learn more about escrow and how it works.

Why Did My Escrow Payment Increase?

Escrow payments may increase if the cost of homeowners insurance or property taxes rise.

An annual escrow analysis is typically performed to determine whether the account has enough funds to cover upcoming payments. If costs increase, monthly escrow payments may also increase to maintain sufficient balance. Learn more about escrow payment changes.

FAQs About Homeowners Insurance

Can My Lender Cancel My Homeowners Insurance?

Mortgage lenders typically cannot cancel a homeowner’s insurance policy directly. However, if you let your insurance coverage expire, lenders may obtain force-placed insurance to protect the property.

What Happens If My Insurance Company Drops Me?

If an insurance provider decides not to renew a policy, homeowners may need to obtain coverage from another insurer before the existing policy expires.

It is in your best interest to not let your insurance coverage lapse. Lender-placed insurance (LPI) is commonly more expensive than a policy you might buy yourself, and often doesn’t cover liability or personal property.

Can I Change Insurance After Closing?

Homeowners are typically able to switch insurance providers after closing, as long as the new policy meets the lender’s coverage requirements.

“Switching homeowners insurance providers is usually a straightforward process,” Madick said. “As long as the new policy is active before the previous one is canceled, homeowners can avoid a gap in coverage. If the policy is escrowed through a mortgage servicer, an insurance agency like Matic can typically assist in coordinating with the servicer to update billing.”

What is Matic and How Can It Help Me?

Matic is an online insurance marketplace that features upwards of 60 A-rated insurance carriers. We’ve partnered with Matic for your convenience so you can compare lenders and get quotes at the click of a button.

Get Started with Matic

Do I Need Homeowners Insurance If I Own My Home Outright?

If there is no mortgage on the property, homeowners are not always required to maintain insurance. However, many homeowners still choose to carry coverage to protect their investment.

Is Homeowners Insurance Tax Deductible?

Homeowners insurance is generally not tax deductible for primary residences. However, different tax rules may apply for rental or investment properties. Contact your licensed tax professional for more information.

Newrez Is Here to Support You

Homeowners insurance plays a major role in protecting both your home and your long-term financial wellbeing. When you understand how coverage works with your mortgage, what’s included in a standard policy and why costs typically shift over time, you’re better equipped to make smart decisions about your home.

Whether you’re buying your first home or taking a fresh look at your current coverage, having a clear picture of your insurance options could bring you real peace of mind.

At Newrez, we want you to feel empowered with knowledge and supported by experts. If you’re in the market for a mortgage, we’d be glad to show you the possibilities.

Newrez analyzed approximately 1.2 million residential mortgage loans that it serviced and that were escrowed for preferred (non-lender-placed) homeowners insurance across two periods: December 31, 2016 through December 31, 2020, and December 31, 2021 through December 31, 2025. Premium data reflects annual homeowners insurance premiums disbursed from borrower escrow accounts, measured as of the final day of each calendar year (December 31). Lender-placed insurance was excluded because of its materially higher cost and non-comparable nature. To improve comparability across periods, the 2016–2020 analysis included loans originated in 2015 or later, and the 2021–2025 analysis included loans originated in 2020 or later.

This analysis reflects the composition of the Newrez-serviced portfolio and is not intended to represent the entire U.S. homeowners insurance market. Newrez reviewed all 50 states and the 20 most populous metropolitan statistical areas (MSAs), based on 2024 U.S. Census Bureau population estimates. MSA averages were calculated using loan-level data tied to borrower ZIP codes and mapped to MSAs using U.S. Census Bureau definitions, as provided by StatisticalAtlas.com. Percentage increases were rounded to the nearest whole number; where rounded values were the same, rankings were determined using the underlying percentage increase carried to two decimal places.

*Average savings are based on 2025 data provided by Matic and reflect the difference between prior and new insurance premiums for Newrez customers who switched carriers through Matic and for whom prior premium information was known to Matic.

Matic is a registered trademark of Matic Insurance Services Inc. Insurance services provided by Matic Insurance Services, Inc., CA License No. 0192444. 585 S Front Street 300, Columbus, OH 42315. 833-471-1876. Quotes are estimates only. Quotes are subject to change without notice. Your actual rate, payment and coverage may be different. Quotes do not constitute an offer of insurance, nor is any contract, agreement, or insurance coverage implied, formed or bound by the provision of quotes. Insurability, final insurance premium quotes and an offer of insurance, if any, will be determined by the insurance company providing your insurance policy. Insurance products may not be available in all states.