If you’re a homeowner, your mortgage likely includes an escrow account to cover property taxes and homeowner’s insurance. These payments can fluctuate, and while they often increase, your escrow account might occasionally hold more than needed. In that case, you could receive a refund, commonly referred to as a “surplus.”

In this article, we’ll explain why escrow surpluses happen and how refunds are issued.

Want to learn more about how your escrow account works? Read this article.

Your Escrow Analysis Might Lead to a Refund

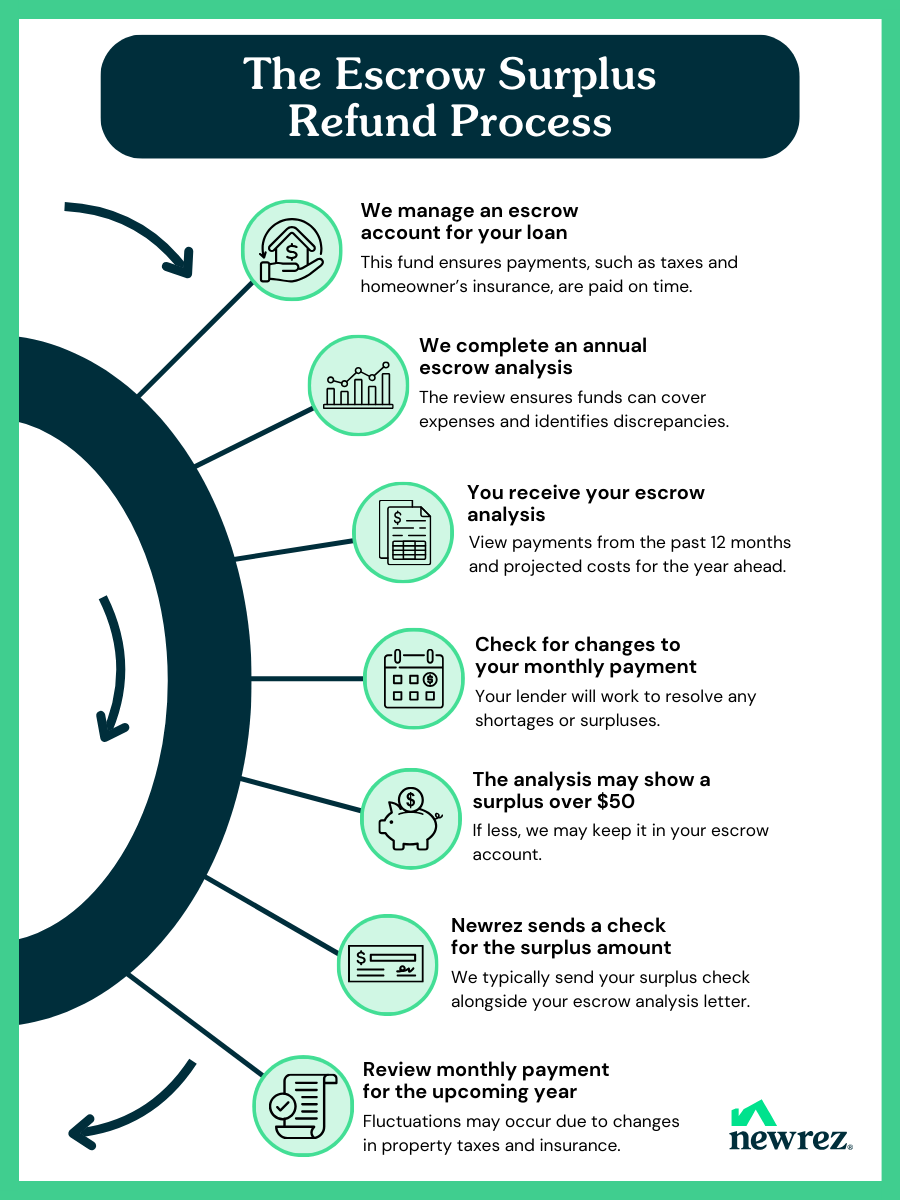

Newrez analyzes your escrow account at regular intervals (typically annually) to make sure there’s enough in your account to cover your property tax and homeowner’s insurance bills due within the upcoming 12 months. In addition to the annual analysis, you can also request an escrow analysis at any time.

During your escrow analysis, we’ll review your tax and insurance bills and compare them to the amount being held in your account. We typically maintain a minimum balance of no more than two escrow payments to help cover unexpected increases in your taxes or insurance premiums. This is referred to as a “cushion.”

If there is a shortfall, we will increase your monthly payment to ensure we have sufficient funds for upcoming tax and insurance bills. However, if your escrow account contains more money into your account than is needed to pay your upcoming tax and insurance bills, your analysis may result in a surplus. For more information about escrow payment changes, read: Why Did My Escrow Payment Change?

Click image below to enlarge.

Why Might I Have an Escrow Surplus?

On occasion, tax or insurance bills will decrease, resulting in you having more money in your escrow account than is needed to pay those bills and maintain your 2-month cushion. If you have an escrow surplus of more than $50, we’re required by law to return that money to you.

Notable exceptions: If the mortgaged property is located in New York, Maryland or Nevada, different options may be available to you. Your surplus also may not be returned to you if you are delinquent in your payments.

Reasons for an Escrow Refund:

· Overestimation of Expenses: When projected costs for taxes and/or insurance exceed the actual amounts paid during the time period from the last analysis to the current analysis.

· Adjustments in Taxes or Insurance Premiums: Changes in rates or billing schedules can result in an escrow surplus.

How Are Refunds Received?

We’ll tell you about the results of your escrow analysis by emailing you a personalized video. We’ll also mail you a detailed letter. If you are to receive a refund, your surplus check will be mailed alongside this letter (with exceptions noted above).

What If There’s a Mistake in My Escrow Account?

It’s unusual but possible for an error to occur with your escrow account. If you suspect an error, reach out to us through the chat function on your online account dashboard or via the contact us page on our website. We are glad to offer assistance with any issues.

We’re Here to Help

Your escrow account enables you to pay your property tax and homeowner’s insurance bills in monthly payments as a part of your mortgage payment, rather than having to remember to pay a larger annual or biannual payment. If you have any questions about the amount held in your escrow account, we’re glad to perform an analysis and provide the results to you.

Thinking about refinancing† to save money or get cash? Talk with a Newrez expert to explore your options.