Looking for ways to reach your financial goals? Maybe you’re hoping to pay down high-interest debt or cover the cost of a college education. If you’re a homeowner, you may have the option to tap into your home’s equity to access cash. One popular way to do this is by getting a Home Equity Line of Credit (HELOC)^, so you can draw cash when the need arises up to your available limit.

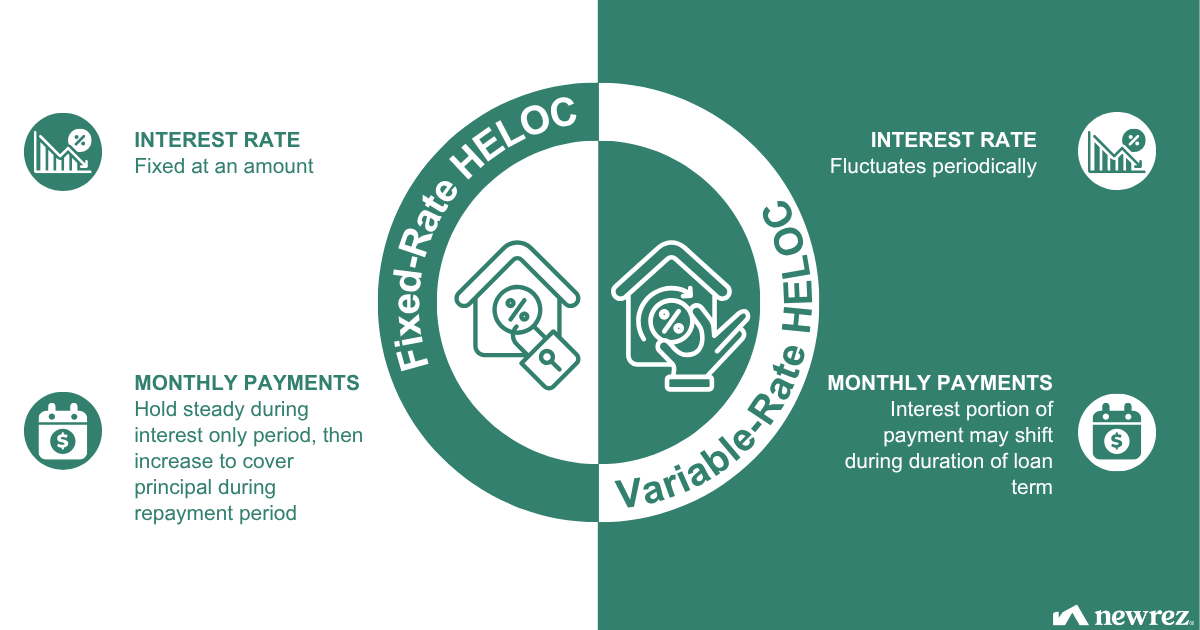

If you’ve heard the term “fixed-rate HELOC,” this refers to a HELOC that holds your interest rate steady for a period of time. While Newrez currently does not offer fixed-rate HELOCs, it's a good idea to stay informed about how different HELOCs work to make the best decision for yourself. Here's a quick guide to understanding these products.

HELOC Basics

A Home Equity Line of Credit is a revolving line of credit secured by your home’s equity. It has two phases:

- Draw Period: During the first 3 to 10 years of your HELOC, you can borrow money up to your approved limit. HELOCs also typically feature an “interest only” period during which you only pay interest. Newrez’s HELOC interest only period is the same as its draw period.

- Repayment Period: During the next 10 to 20 years, you are not allowed to make any more draws, and instead repay the principal amount you used with interest.

For a typical HELOC, the interest rate usually shifts throughout the term based on the movement of the prime rate published daily in The Wall Street Journal®.

HELOCs may enable you to hit your financial priorities, whether you’re hoping to complete home improvements, cover emergency expenses or fund a wedding. Reach out to one of our mortgage experts to find out about Newrez’s HELOC product.

How Does a Fixed-Rate HELOC Differ?

A fixed-rate HELOC may allow you to lock in your interest rate, rather than having a variable rate.2 Some fixed-rate HELOC products may even allow you to unlock to a variable rate if rates drop.

However, fixed-rate HELOCs may carry some drawbacks. Here are some things to keep in mind:

- P&I Payments: Once you elect to fix your rate, you may have to make both principal and interest payments, rather than paying interest only during your draw period.

- Fees: Locking in your interest rate traditionally comes with a corresponding fee. Additionally, some lenders may charge a penalty if you pay off the balance early.

- Lock Limits: Lenders may also set limits on the number of times you can lock your rate.

Find the Loan That Works for You

Your home equity is yours to use, and it can be a great tool for addressing your cash needs. A HELOC can grant you a great deal of flexibility in drawing your equity on your own timeline during the draw period. But you should also know that HELOCs aren’t your only option for accessing equity. If you’d prefer to access a lump sum of cash upon closing and make predictable payments, you may want to explore a home equity loan††. Or you can roll it into your existing mortgage payment by taking a cash-out refinance.†

If you’re not sure where to start, Newrez’s mortgage experts are glad to answer your questions and present you with options. Reach out today.

References:

2HELOC Fixed-Rate Option: What It Is, How It Works

The Wall Street Journal® is a registered trademark of Dow Jones & Company, Inc. and is not affiliated with Newrez LLC.