Every homeowner is unique—with their own lifestyle, preferences and plans for the future. That’s why mortgage loans come in all shapes and sizes, offering different features, requirements and payment structures. Below we’ll walk you through the basics to help you explore which type of loan could be the right fit for your needs.

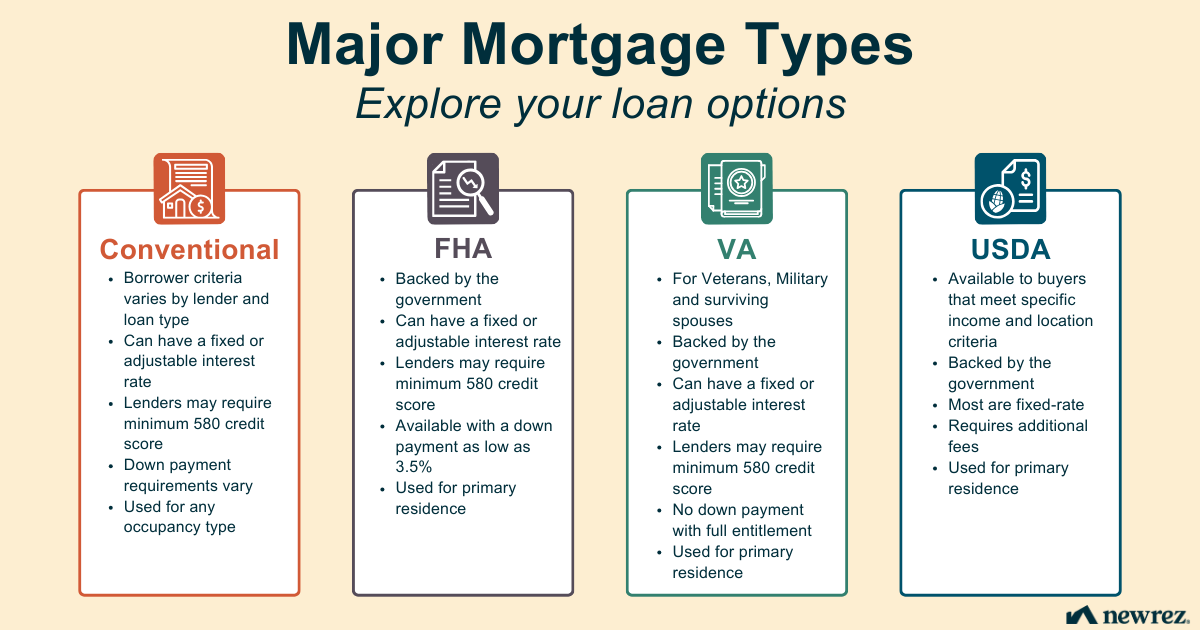

Mortgage Loan Types

The loan type you choose could depend on factors such as your financial circumstances, where you live, how you’re employed, whether you are a Veteran or member of the Military and whether you plan to live in the home you’re purchasing.

Click image below to enlarge.

Conventional Loans

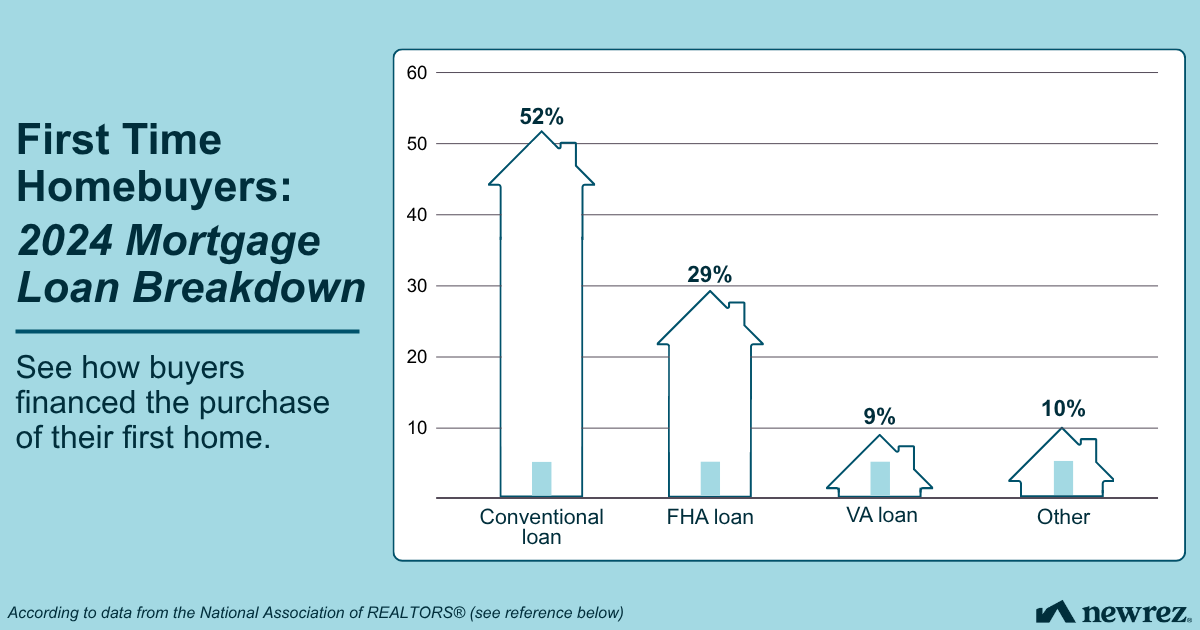

In 2024, the majority of homeowners elected to finance their home with a conventional loan.1 These loans are offered by private lenders, many of them purchased by the government-sponsored enterprises Freddie Mac® or Fannie Mae®. Private lenders set the credit and income requirements.

Key Features:

- Often require credit scores of 580 and upward

- Down payments as low as 3%, though putting down 20% or more is typical.

- You may avoid having to pay for private mortgage insurance (PMI) if you put down 20% or more.

- Can be used for primary, secondary or investment properties

Government Loans

These loans are designed to make homeownership more accessible to certain groups of people such as Veterans, rural populations or low-income households. They’re provided by private lenders but guaranteed by the government, which generally makes it easier for lenders to approve borrowers with less-than-perfect credit or those who can’t afford to make a large down payment.

Federal Housing Administration (FHA) Loans

These loans are designed for those with imperfect credit or who may not have ample savings for a down payment, including first-time homebuyers.

- Down payments as low as 3.5%

- Often requires minimum credit score of 580

- Flexibility on debt-to-income (DTI) ratio

- Require upfront mortgage insurance premium (UFMIP) or annual mortgage insurance premium (MIP)—upfront MIP is typically 1.75% of the loan amount while annual MIP is paid monthly as part of your mortgage payment

Learn more about FHA loans here.

Department of Veterans Affairs (VA) Loans

These loans are meant to help Veterans, active-duty Military and surviving spouses achieve homeownership.

- Eligible borrowers may be able to put zero money down

- No private mortgage insurance (PMI) required

- May include a VA funding fee

- Competitive interest rates

Learn more about VA loans here.

U.S. Department of Agriculture (USDA) Loans

These loans are tailored to low-to-moderate income borrowers in rural or suburban areas.

- Eligible borrowers may be able to put zero money down

- May offer lower interest rates than available for conventional loans

- Must meet income requirements based on the county where you live

- Requires an Upfront Guarantee Fee, which is 1% of the loan paid at closing or rolled into the loan

- Requires an Annual Guarantee Fee, which is .35% of the remaining loan balance paid monthly as a part of your mortgage payment

Non-Qualified Mortgage (Non-QM) Loans

Lenders sometimes offer loans that fall outside traditional conventional loan requirements. Newrez offers a series of non-QM loans for qualified borrowers in unique circumstances, including:

- Loans for self-employed professionals looking to qualify without the use of a W-2 for income verification

- Loans for borrowers who have experienced derogatory credit events, such as a bankruptcy or foreclosure, who would like to get a jumbo loan

- Loans for real estate investors wanting to qualify by demonstrating cash flow

Reach out to a Newrez mortgage expert to find out if you qualify.

Loan Terms: 30-Year vs. 15-Year Mortgages

Whether you want a 30-year mortgage or 15-year mortgage will depend on whether you’re prioritizing lower monthly payments, or cutting down on interest costs and owning your home outright on a shorter timeline.

30-Year Fixed Mortgage

- Lower monthly payments

- Higher total interest over the life of the loan

- May be beneficial for long-term budgeting and flexibility

15-Year Fixed Mortgage

- Higher monthly payments

- Lower total interest cost over the life of the loan

- May have lower interest rates than 30-year terms

Interest Rate Types: Fixed vs. Adjustable

Many homeowners prefer the predictability of a mortgage with a fixed interest rate, but in some circumstances borrowers may save money with an adjustable-rate mortgage.

Fixed-Rate Mortgage (FRM)

- Interest rate remains stable for the life of the loan

- Predictable monthly payments

- Ideal for long-term homeowners

Learn more about fixed-rate loans here.

Adjustable-Rate Mortgage (ARM)

- Fixed rate for an initial period (ex: 5, 7 or 10 years)

- Then adjusts every six months or one year based on market indices, though increases may be capped

- Lower initial rates, but risk of increase after initial period

Learn more about adjustable-rate mortgages here.

ARM Considerations:

- May be suitable for short-term homeowners or those expecting income growth

- Risk of payment shock if rates rise significantly

Risky Loan Features to Look Out For

When you apply for a loan, be sure you clearly understand the payment and fee structure so you aren’t caught off guard.

- Balloon Payments: Large lump-sum payments at the end of the loan

- Negative Amortization: Payments don’t cover interest, and unpaid interest is then added to the loan’s principal amount, increasing how much you owe

How to Compare Loans: The Loan Estimate

Every lender is required to provide a standardized loan estimate within 3 days of your application. You can use it to compare monthly payments, interest rates, closing costs and more.

Still have questions about what loan might be right for you? At Newrez, our goal is to support you throughout your homeownership journey. Our mortgage experts are glad to walk you through your options.

Fannie Mae® is a registered trademark of the Federal National Mortgage Association. Freddie Mac® is a registered trademark of the Federal Home Loan Mortgage Corporation.

References: