A VA home loan offers qualified Active-Duty Military servicemembers, Veterans and eligible surviving spouses an affordable path to homeownership.

Click to navigate:

VA Loan Eligibility Requirements

Certificate of Eligibility (COE)

Financial Preparation for a VA Mortgage

Income and Employment Documentation

The VA Funding Fee

Closing Costs

Property Requirements

FAQs

Conclusion

We at Newrez pride ourselves on bringing excellent service to our Military borrowers. If you’re new to VA loans, we’ve provided this article as a guide so you’re prepared to move through the process efficiently. If you have further questions about VA loans, our mortgage experts would be happy to guide you through the process.

Confirm VA Loan Eligibility Requirements

To qualify for a VA loan, you must meet minimum service requirements based on your Military status:

- Active-Duty Servicemembers: At least 90 consecutive days of service.

- Veterans: Eligibility varies by service era and discharge status—most who completed their term qualify.

- National Guard: 90 days of qualifying Active-Duty service (with at least 30 days consecutive) under Title 10 or Title 32 orders, or 6 creditable years with honorable discharge.

- Reserves: 90 days of Active-Duty under Title 10 orders, or 6 creditable years in the Selected Reserve with honorable discharge.

- Surviving Spouses: May qualify under specific circumstances outlined by the VA.

For full details, check the VA’s official eligibility guidelines.

Certificate of Eligibility (COE) Checklist

A COE confirms your VA entitlement. You can obtain your COE from:

- Your Newrez loan officer

- VA eBenefits portal (sign in here)

- VA Form 26-1880 (mail-in option)

Documents needed to obtain your COE:

To get your COE, you’ll have to provide documentation that proves your service.

- Veterans: Provide copy of your discharge or separation papers (DD214).

- Active-Duty Servicemembers: Obtain a statement of service signed by your commander or personnel officer.

- Current or Former Activated National Guard or Reservist: Provide your annual point statement and your DD214.

- Current Reservist or National Guard, Never Activated: Obtain a statement of service signed by your commander or personnel officer.

- Discharged National Guard, Never Activated: Provide your Report of Separation and Record of Service (NGB Form 22) for each period of service, as well as your Retirement Points Statement (NGB Form 23).

- Discharged Reservist, Never Activated: Provide a copy of your latest annual retirement points and proof of your honorable service.

- Surviving Spouse: If you qualify, you’ll need to provide your spouse’s DD214, if available. If you’re receiving Dependency and Indemnity Compensation (DIC), you’ll have to fill out VA Form 26-1817. Otherwise, fill out an application for DIC, VA Form 21P-534EZ, and provide them to us with a copy of your marriage license and your spouse’s death certificate.

Financial Preparation for a VA Mortgage

When you apply for a VA loan with Newrez, we will look over your income, assets and credit profile. You may qualify for a VA loan with us with a:

- Minimum 580 credit score

- Documented employment history (see below for required documents)

- No recent (within 2 years) derogatory credit events, such as a foreclosure or bankruptcy

- Debt-to-Income ratio of 55% or lower (may be higher if you meet other criteria)

Before you apply, it may be a good idea to review your credit to be sure there aren’t any errors in the report. If you’re able, try and pay down debts prior to applying for a mortgage. Focus first on any lines of credit where you’re close to your credit limit. Avoid opening new lines of credit during the application process.

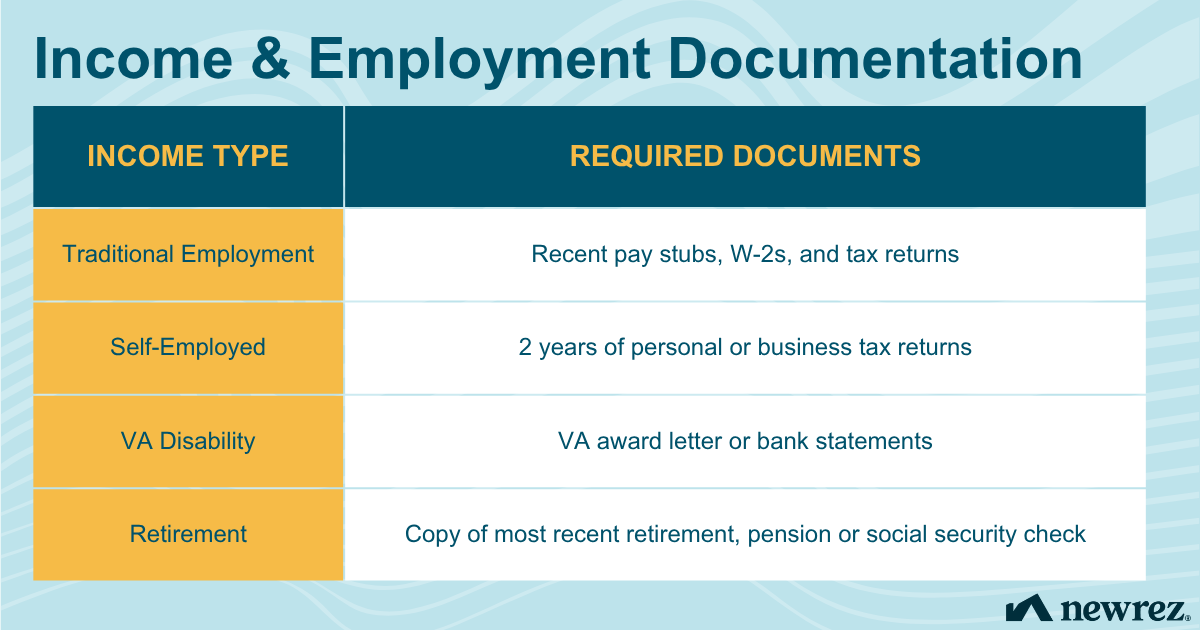

Income and Employment Documentation

We verify stable income to ensure borrowers can repay the loan. You’ll first have to fill out IRS Form 4506-C, which gives us permission to obtain income information about you. Active-Duty Military will also need to provide their Leave and Earnings Statement (LES). From there, required documents typically include:

Click image to enlarge

While VA loans require $0 down with full entitlement, borrowers should still prepare to pay a VA funding fee. This one-time charge helps keep the VA loan program running and typically ranges from 0% to 3.3% of your total loan amount. The exact percentage depends on a few key factors:

- Whether you're purchasing or refinancing

- How much you're putting down

- Whether it's your first time using your VA loan benefit

Who’s Exempt from the VA Funding Fee?

Not everyone has to pay this fee. You may be exempt if:

- You have a service-connected disability

- You're a surviving spouse receiving Dependency and Indemnity Compensation (DIC)

- You've received a Purple Heart

- You have a proposed or memorandum rating for compensation due to a pre-discharge claim

If you do need to pay the fee, you’ve got options: roll it into your loan and pay it off over time, or pay it upfront at closing.

Beyond the VA funding fee, there are standard closing costs to budget for. These can include:

- Origination fees

- Discount points

- Appraisal fees

- Title insurance

- Recording fees and more

Property Requirements Preparation

Because the VA guarantees the loan, properties must meet Minimum Property Requirements (MPRs). The process goes like this:

- A VA-approved appraiser will assess the property’s condition and value. The home must be structurally sound and sanitary.

- Our VA underwriter will review the appraisal and issue a Notice of Value. If the property meets VA standards, the loan process continues as normal. If an issue is found, additional inspections may be needed, repairs may be required, or you may need to search for a new property.

Can I get a VA loan with no down payment?

Yes, VA borrowers qualify for 0% if they have full VA entitlement. Sometimes, VA borrowers can put 0% down even if they only have partial entitlement—reach out to a Newrez mortgage expert for details.

Do VA loans require PMI?

No. VA loans do not require monthly PMI, which lowers long-term costs.

Do I need perfect credit for a VA mortgage?

No. You may qualify for a Newrez VA loan with as low as a 580 credit score.

Successful VA loan preparation begins before you submit an application. By gathering documents in advance and building a strong financial profile, borrowers could move through the process with greater confidence.

At Newrez, we’re honored to serve those who have served. If you’re a member of the Military or a Veteran and you have more questions about the VA loan, don’t hesitate to give us a call.