VA loans were created by the U.S. Department of Veterans Affairs to help Veterans, active-duty service members and surviving spouses achieve homeownership. Yet misconceptions about VA loans still persist, potentially preventing qualified borrowers from taking advantage of these loans.

If you’re not sure how a VA loan can benefit you, read on – and when you’re ready to explore your options further with Newrez, our mortgage experts will be glad to help.

Understanding VA Loans

Because the VA guarantees these loans, lenders are usually able to offer favorable terms. This may enable qualified borrowers to secure lower interest rates, more flexible qualification requirements and reduced upfront costs compared with a conventional loan.

Myth #1: VA Loans Are Only for Retirees

Some people might be stuck on the notion that VA loans are restricted to Veterans who served for a complete career. In reality, a broad range of people are eligible:

- Active-Duty Military: Those currently serving may be eligible, so long as they meet length-of-service requirements.

- Veterans: Individuals who have completed their term of service often qualify, though the minimum service requirement will typically depend on when you served and the circumstances of your service.

- National Guard and Reserve Members: Many qualify if they have sufficient service time or have been activated under federal authority.

- Surviving Spouses: In some situations, surviving spouses of fallen service members can receive a VA loan.

For specifics on length-of-service requirements, review eligibility requirements on the VA’s website.

Myth #2: You Need Excellent Credit to Qualify

If you have less-than-perfect credit and you’re worried how this might affect your chances of qualifying for a VA loan, you should know that these loans carry quite flexible credit guidelines. Lenders set their own minimum credit score requirements, but often they’re able to be more flexible with VA loan credit requirements as compared with conventional loans.

Myth #3: A Down Payment Is Required

One of the biggest benefits to VA loans is that they enable borrowers to buy a home even if they put zero money down. This differs from conventional loans, which often require a minimum percentage of the purchase price up front. VA loans stand out by:

- Allowing 0% Down: Qualified borrowers could save thousands in upfront costs.

- Eliminating Private Mortgage Insurance (PMI): Typically, borrowers who put up a low down payment are required to pay PMI to reduce the risk to the lender. VA loans don’t require monthly PMI, potentially lowering monthly costs.

Enabling no money down may make homeownership more attainable to Military families with limited savings.

Myth #4: The VA Funding Fee Is Too High

Potential borrowers might have concerns about the VA funding fee, which helps keep the program afloat. While there is a fee involved, the amount varies based on several factors including the down payment size, whether it’s a purchase or refinance and whether the borrower has used a VA loan previously. Some individuals (often those receiving disability compensation) may be exempt from paying the fee.

Borrowers may be able to roll this fee into their mortgage, minimizing costs at closing.

Myth #5: VA-Approved Properties Are Hard to Find

While the VA loan program does have Minimum Property Requirements (MPRs), these are focused on the important criteria of health, safety and structural integrity. Many homes, both brand new and existing, meet these qualifications for habitability. Work with a lender and a real estate agent to make the process smoother:

- Pre-Approval**: Secure your eligibility and know how much house you can afford.

- Property Inspection: Ensure the home meets VA standards.

- Appraisal: A VA appraiser evaluates the market value and general condition of the property.

Myth #6: VA Loans Take Too Long to Close

Once you have your heart set on a home, it’s understandable that you’d be eager to get the closing process over with. Modern processes and automation now enable VA loans to close on timelines similar to those of conventional loans. Closing times have averaged from 30 to 51 days over the last six months at Newrez.

Delays can occur when complete documentation hasn’t been provided or other issues occur, but these challenges aren’t unique to VA loans. You can help the closing process move smoothly by having documents ready and having open communication with your lender.

Myth #7: Refinancing† With a VA Loan Is Pointless

VA loans offer robust refinancing options, including Interest Rate Reduction Refinance Loans (IRRRL), which can lower the interest rate and monthly mortgage payment. Some borrowers save significantly each month via streamlined refinances that don’t require much paperwork. On top of that, certain refinance options enable borrowers to turn their home’s equity into cash, which can be used for home improvements or debt consolidation.

Learn more about VA refinance and purchase options in this article.

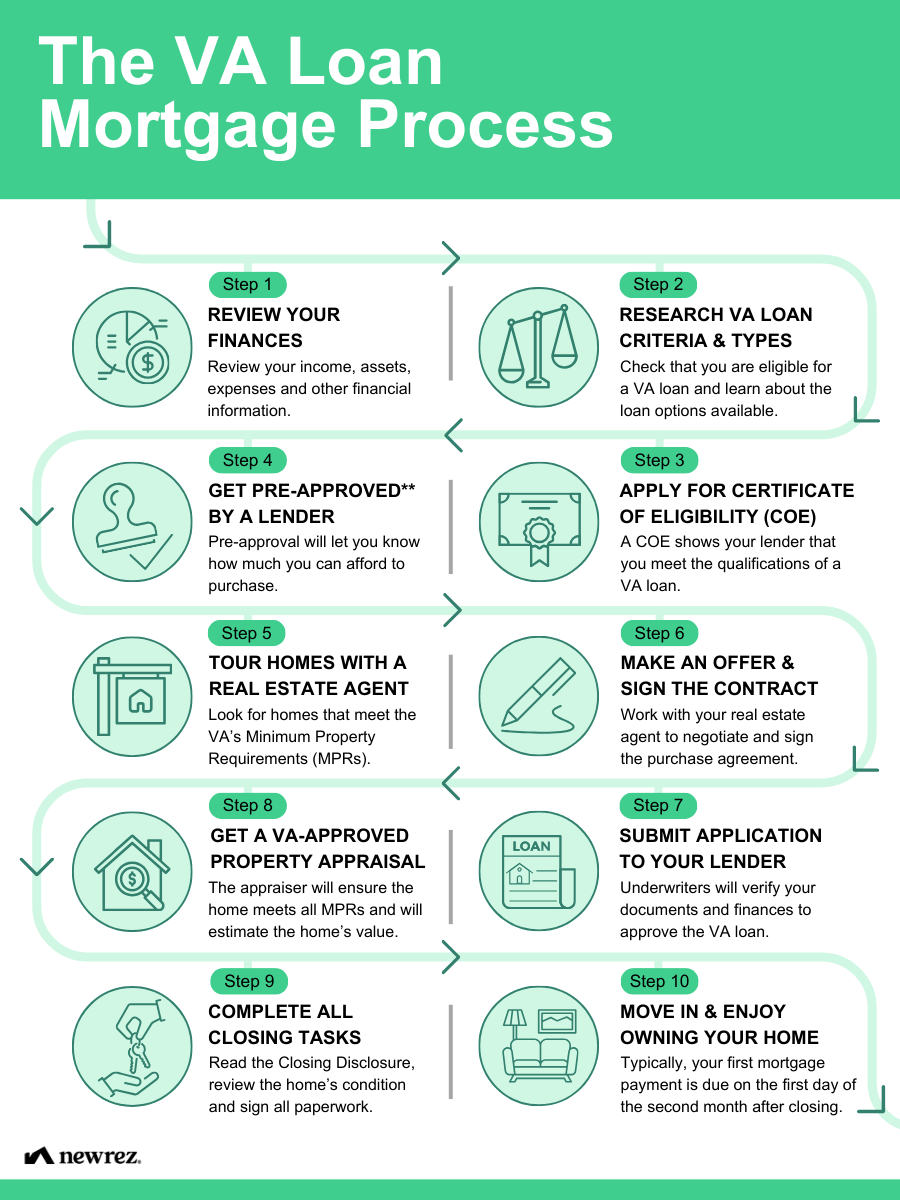

How to Navigate the VA Loan Process

If you’re thinking about applying for a VA loan, be sure to talk through the process with a mortgage expert. Here are some general steps:

Newrez Supports Veterans and Active Duty Military

VA loans can provide powerful homeownership opportunities for those who have served our country. At Newrez, we pride ourselves on our service to those who have served. Our mortgage experts care about helping you achieve homeownership.